Happy New Year, everybody! The year has started off on a very strange note. First, New Year’s Day was on a Wednesday. It felt odd. Then, the horrific fires devastated Pacific Palisades, Altadena, and other nearby areas. Almost beyond belief.

Then, a day of mourning for President Carter shut down markets, followed by the Prime Minister of Canada resigning. Interest rates jumped, and the stock market sold off, then bounced back. The inauguration fell on a national holiday. I don’t recall that happening, but it might have.

Like I said, it has been a strange start to the new year. Let’s keep our fingers crossed that things settle down, and we can start to see blue skies again.

We get questions all the time from clients, and in some cases, more than one person might have the same question. So, I’ll do a little Q&A.

My daughter just landed a good job. What advice do you have for her regarding finances?

If I were to give just one piece of advice, I’d tell her to get rich slowly. That entails an unwavering plan to put away money consistently. I’d also remind her that to be rich is to be content.

If I just bought a stock, and it immediately falls 10%, what should I do?

If you bought it for speculation, I’d sell it. It didn’t work. Your first loss is your best loss. If you bought it for an investment, hang on to it and consider adding more. This is, of course, if you have researched it, and the company has a good balance sheet, growing revenues, and is profitable.

What do you advise for the highest percentage of one particular stock in a portfolio?

There are two schools of thought here: Don’t put all your eggs in one basket, or put all your eggs in one basket and watch the basket closely. Our firm manages money for clients using the former. Diversify and keep no more than 5-7% in any one holding.

I watch the markets and get frustrated by the wild swings in the value of my portfolio. Any suggestions?

If I’ve said this once, I’ve said it 100 times: If you want to reduce the volatility in the market, don’t look at it so often. That really works. So, unless you are a day trader, watching the market every hour is just going to cause you stress and make you make emotional decisions, which usually aren’t good. Have a plan, stick with the plan unless your circumstances change, stay diversified, and own quality. That tends to work over longer periods.

Last question: What is your expectation for inflation in the coming year?

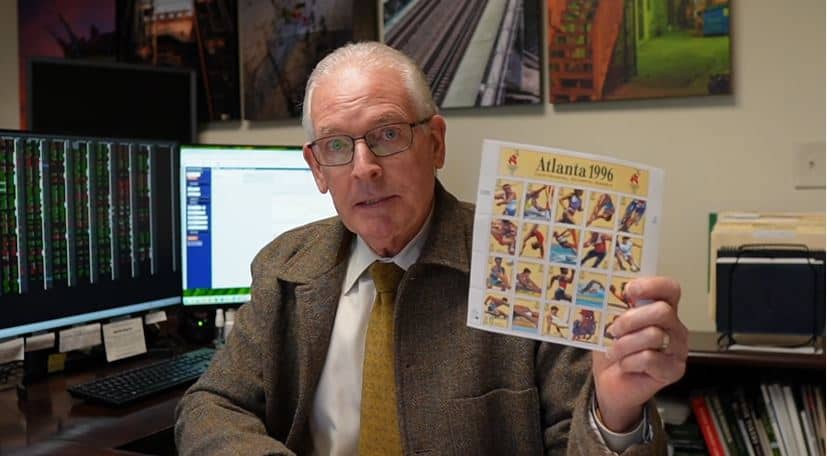

I think it is going to be higher, and the prices we see now are going to be sticky, meaning they probably won’t come down unless we go into a recession. Here is an interesting way to look at inflation—not the CPI or the PCE that the Federal Reserve looks at—it is the price of a stamp. The cost to send a first-class, regular-size envelope from where you live to anywhere in the United States. Back in 1996, a first-class stamp was 32 cents. Today, a first-class stamp is 73 cents. The inflation rate for the stamp is 3.5%. I think that is a good way to measure longer-term inflation.

If you have any questions, please don’t hesitate to call. Until next time, I’m Phil Albitz. Thanks for watching.